Smoooth

Klarna is the world-leading provider of buy-now-pay-later checkouts; they offer shoppers the ability to defray a large purchase over multiple installments. Part of the value proposition is that many ecommerce customers, especially Gen Z, don't have credit cards - but Klarna provides an equivalent service much more easily.

In the past, businesses that offered a service like this tended to make money from charging fees to users; it's the crucial revenue stream for payday loan providers, and is also important to credit card providers. Klarna, however, wants to make money by charging transaction fees to merchants; in 2020 they derived just 15% of their revenue from interest on late payments, and their goal is to get that figure to zero. That's in line with their biggest competitor, the Australian fintech Afterpay (which was acquired by Square in August 2021 for the equivalent of $29bn), which also derived 15% of its revenue from interest payments in FY20.

These revenue streams aren't really complementary - instead, they cannibalise each other, which explains the reasoning behind Nollmissionen. 85% of Klarna's revenue comes from transaction fees, and so the more transactions they have, the more revenue they receive. While Klarna has to borrow capital from institutions like Goldman Sachs at 2% to fund their consumer credit provisions, they can earn up to a 50% return on capital by using that capital to fund up to 25 transactions a year, and then making a gross margin of about 2% on each of those transactions.

As such, it's crucial for Klarna to get as many transactions flowing through their pipes as possible, so that they can repeatedly skim off 2%. Their dream customer is a teenage girl buying clothes with Klarna and reselling them on Depop; the transaction frequency and consistency she generates leads to massive profits. If the public starts to see Klarna in the same light as Wonga and QuickQuid, predatory payday lenders charging enormous APRs who generated a huge amount of negative publicity (and FCA regulation) around 2013-2014, then transaction volumes will fall. Although reducing the burden of late fees may bring an increased risk of fraud, it certainly has the potential to drive continued revenue growth.

The logic behind charging merchants instead of customers is that BNPL services get users spending more. Brands pay a premium to get an increased share-of-wallet (SOW) through increasing average order value (AOV) and transaction frequency. This makes sense - BNPL makes it easier to spend in certain areas, so people spend more there. People choose to devote more of the money they have to spending on fashion, cosmetics, tech and so on.

But does this actually happen? Do users really spend more? Personally, I'm convinced that they do - I believe in BNPL as a mechanism, as do most people I speak to. But Klarna still has to convince merchants to use their checkout function, with its concomitantly higher fees, and it does this by pointing to evidence, in aggregate and in individual case studies, that Klarna increases AOV.

This second example comes from Klarna's March 2020 "Fast-track Upturn" report; it sketches an example of how Klarna might increase a business's revenue through increasing AOV like in the individual case studies.

However, a simple statistical trick that lies behind all this; users are more likely to use Klarna on their most expensive purchases; this is plausible because while it's always economically rational for an individual to take advantage of Klarna's BNPL services, which function as an interest-free loan, they might not bother to do so for small purchases. That means that there is a powerful selection bias that means that the purchases using Klarna's payment method have a much higher AOV than those that don't.

We can show this using an example:

Imagine a business normally sees 100,000 transactions at a price uniformly distributed between £0 and £100.

Now imagine that Klarna comes along.

30% of the users who spend more than £75 decide to use Klarna to spread out the cost of their purchases, and none of those who spend less than £75 bother to do this.

That would look a bit like the diagram below - if the x-axis represents the AOV, the pink area shows the % of transactions processed by Klarna as opposed to non-BNPL checkouts.

You can think of alternative models, but the point is that the centre of mass of the pink area, which corresponds to the AOV of Klarna's transactions, will always be further to the right than that of the grey area. We can quickly simulate the effects of the first model using R.

set.seed(1)

#Generate 100,000 transactions uniformly distributed between £0 and £100

spends <- data.frame(runif(100000, min = 0, max = 100), runif(100000)) %>%

setNames(c("base", "check")) %>%

#Pass 30% of the transactions over £75 through Klarna's checkout

mutate(klarna = ifelse(base > 75, 1, NA)*ifelse(check < 0.3, 1, NA)*base)

spends %>% summarise(mean(base))

#AOV for all transactions = £49.96

spends %>% filter(!is.na(klarna)) %>%summarise(mean(klarna))

#AOV of Klarna's transactions = £87.53

spends %>% filter(is.na(klarna)) %>%summarise(mean(base))

#AOV of the remaining transactions = £46.87

In the world generated by these not-entirely-unreasonable assumptions, Klarna processes just 7.6% of the transactions, and haven't increased the merchant's revenue at all, but they can still claim to have increased AOV by 87%! In spite of what they claim, Klarna would have simply cannibalised a business's most valuable transactions and charged higher fees for them.

Case Studies

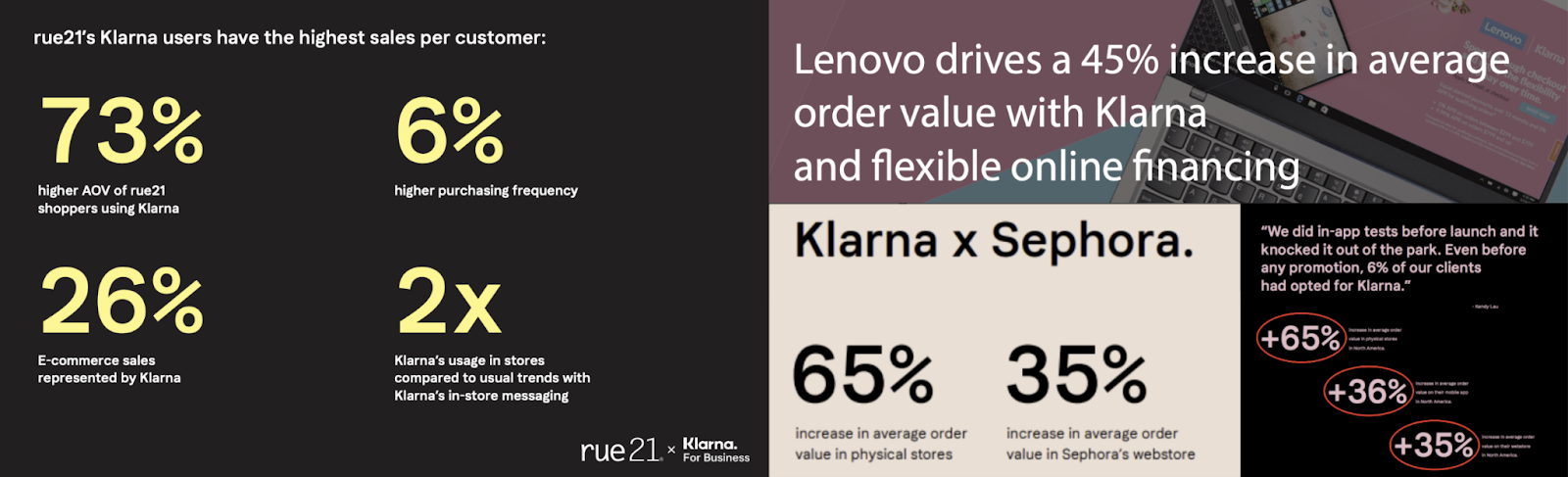

This genuinely does seem to be how Klarna is calculating their numbers; see this example from their Lenovo case study:

In fact, Lenovo has enjoyed an increased AOV of 45% on purchases made via Klarna compared to its other payment methods. Compute that.

We have! Conditioning simply on the payment method used doesn't work. Here's another one from their Pangaea case study:

Additionally, incorporating interest-free instalment plans can have a significant and long-lasting impact on your average purchase price too. Merchants who offer this option also saw 68% higher AOV on purchases made in interest free instalments.

When you look back at their case studies, most of the numbers they cite are probably the product of selection bias.

Real Evidence

In order to generate convincing causal evidence of incremental revenue increase - i.e. "sales driven by the publisher, that the advertiser would not have otherwise received." - Klarna would have to do some of these things:

Compare AOV at businesses before and after they started using Klarna, accounting for seasonality.

Compare AOV at businesses on and off Klarna.

Run A/B tests where some users are not given the option to use Klarna at checkout.

Segment customers by whether they used BNPL, and compare the AOV of those segments.

In another report, also on Lenovo, Klarna actually did an A/B test:

Lenovo ran an A/B test for three weeks to measure impact between a test group of customers shown dynamic on-site messaging about instant financing against a control group of customers who weren’t.

Those in the test group had a 25% higher average order value as compared to the control group. This, combined with a nearly 40% increase in the Klarna share of Lenovo sales with the implementation of the messaging, confirms the incremental value this solution delivers to merchants.

This test may still not be perfect, but at the very least it compares users, not transactions, with each other. The fact that they get a smaller but still significant positive effect underlines my original point. Klarna works because consumers want BNPL - but their results aren't quite as effective as their marketing would have you believe.