Cannibals, Brokers, and Sponsors

One of my favourite mental models is Chesterton’s fence. If you can’t figure out why something exists, you absolutely shouldn’t get rid of it; instead, you should understand why it was put there in the first place, think about whether that reason is still a good reason, and then decide if you should get rid of it.

It meshes closely with Des Traynor’s approach to building AI products:

“I think you need to work out if there are core product assumptions that are just no longer valid, [and then] you need to put down everything. Nothing else matters. If you get this wrong, nothing else matters. If you get this right, nothing else matters. It's the only thing.”

What assumptions are people making? Why are they making them? And are they still valid?

That attitude is really important for thinking about insurance, because it’s such an old and rich and layered space, full of quirks and idiosyncrasies. At every turn, it’s developed this complexity in order to solve problems.

In 2000, Joel Spolsky, then a PM at Microsoft, wrote an essay called Things You Should Never Do, Part I; the answer being “rewrite the entire codebase”. And it’s for exactly the same reason:

“Back to that two page function. Yes, I know, it’s just a simple function to display a window, but it has grown little hairs and stuff on it and nobody knows why. Well, I’ll tell you why: those are bug fixes. One of them fixes that bug that Nancy had when she tried to install the thing on a computer that didn’t have Internet Explorer. Another one fixes that bug that occurs in low memory conditions. Another one fixes that bug that occurred when the file is on a floppy disk and the user yanks out the disk in the middle. That LoadLibrary call is ugly but it makes the code work on old versions of Windows 95.

Each of these bugs took weeks of real-world usage before they were found. The programmer might have spent a couple of days reproducing the bug in the lab and fixing it. If it’s like a lot of bugs, the fix might be one line of code, or it might even be a couple of characters, but a lot of work and time went into those two characters.

When you throw away code and start from scratch, you are throwing away all that knowledge. All those collected bug fixes. Years of programming work.”

So when you’re approaching the insurance industry, and you think "I don't see the use of this; let us clear it away”, it’s incumbent on you to go away and understand deeply how the current state of affairs came to be.

I mean, obviously, I am a historian, and this is what we were trained to do.

I’m a hammer, and boy do I see a lot of nails.

Shockingly, I keep noticing things that confirm my view of the world.

Anyway, here’s a sketch of the value chain in US commercial insurance broking; how different firms relate to one another, and what they each offer. As with many things, it looks ridiculous at first glance, but I promise there’s an internal logic. I’ve written about the dynamics in insurance broking before, but there’s more to say.

In the United States, insurance is regulated by the states and not by the federal government. This was conclusively ratified by the 1945 McCarran-Ferguson Act (15 USC §1012):

“The business of insurance . . . shall be subject to the laws of the several States… no Act of Congress shall be construed to invalidate, impair, or supersede any law enacted by any State for the purpose of regulating the business of insurance."

The states regulate rate and form: the amount that insurers can charge, the kind of questions they can ask, and the structure of the policy itself. These policies are called admitted, but there’s also a surplus lines market. Any licensed retail insurance broker can get a surplus lines license too, to seek non-admitted, surplus lines insurance policies. These policies might be offered by a non-admitted insurance company (perhaps from another state) or an alien insurance company from outside the US.

California maintains a list of admitted insurers here - there are about 1200 of them. They also maintain a List of Approved Surplus Line Insurers (LASLI), with another 140 insurers. The National Association of Insurance Commissioners maintains a Quarterly Listing of Alien Insurers, with about 70 insurers plus the 70 Lloyd’s syndicates. Companies will appear multiple times on each list: for instance, Chubb has two CA admitted subsidiaries, two on the LASLI, two in the in the QLAI, and a Lloyd’s syndicate.

In order to approach a non-admitted insurer, a broker needs to demonstrate that they’ve tried to get insurance in the admitted market; they typically need to prove that they’ve made a ‘diligent search’, which means getting three declinations from admitted insurers, unless they’re getting a particularly weird kind of insurance, in which case they needn’t bother with the admitted market. The California insurance commissioner lists those here. This is a super fun read: classic autos, kidnap and ransom, sawmills, blasting contractors, hay in the open, security guards, oilfield contractors, tattoo artists - for anything like this, you go straight into surplus lines.

Some surplus lines insurers are based in the US, but many are in London. By accident of history, London is the Silicon Valley of insurance; a self-reinforcing vortex of capital and talent that sucks up most of the biggest and weirdest risks in the world.

To broke admitted P&C insurance, you need a state-issued licence - this works like a driving licence, in that you can use it in other states too. To approach surplus lines insurers, you need an additional licence. And to approach London underwriters, you need to work with a London broker. So to access the three layers of insurer (admitted, surplus, and London), you need three kinds of broker (US retail, US wholesale, and London wholesale). These three brokers partner with each other in a chain, each taking a commission along the way.

Each broking firm chooses where they sit in this value chain. Small brokers specialise in just one of the three functions. Larger brokers can sit across two, or even three of them. Here’s a diagram:

Only about seven firms have US retail, US wholesale, and London operations, not least because each function can cannibalise the others. For instance, a retailer might not want to partner with a wholesaler that is competing with them for retail clients, and a US firm might want to choose a London firm that doesn’t have US operations.

Beyond that, it’s important to understand that individual brokers make decisions about who to trade with on a risk-by-risk basis, informed but not determined by firm-wide strategy. You’d think that Aon retailers would always work with Aon wholesalers in the US and London, but in practice that’s not true. Because brokers stay in the space for their entire career, occasionally moving between firms, the easiest way for an individual to get a deal done is often to phone a friend; in fact, the ability to phone a friend that the rest of the firm doesn’t normally trade with is a key part of the value that experienced brokers bring. Managing this tension is crucial to success - senior brokers have to appreciate how the smaller deals being done by their subordinates affect higher-level relationships, and be willing to bang heads together to get to the right answer.

There are three big wholesale brokers: Ryan Specialty, CRC and Amwins, each of which are valued at about $15bn. They service the ~50,000 small retail brokers, ranging from sole traders to firms with thousands of employees, and help them access surplus lines insurers across the world. A few startups are looking to compete with them - Arqu, Limit, recently Quotewell, and formerly Pathpoint. It’s a brutally difficult space, where network effects mean that scale wins.

Amwins have a London office, but Ryan and CRC have to partner with London brokers in order to get access to the market. Here’s a map of the other firms in the wholesale space:

Some retailers are big enough to justify their own wholesale operation: HUB and Alliant are great examples. Neither of those firms have offices in London, but HUB has a fairly exclusive deal with Ardonagh, and Alliant has the same thing with Howden. This involves some cloak-and-dagger work, setting up secret meetings with brokers and insurers to move business around the market. The division between these firms and the 50,000 other brokers is continuous, not discrete - brokers are making tactical and strategic decisions about when it does and doesn’t make sense to use a wholesaler.

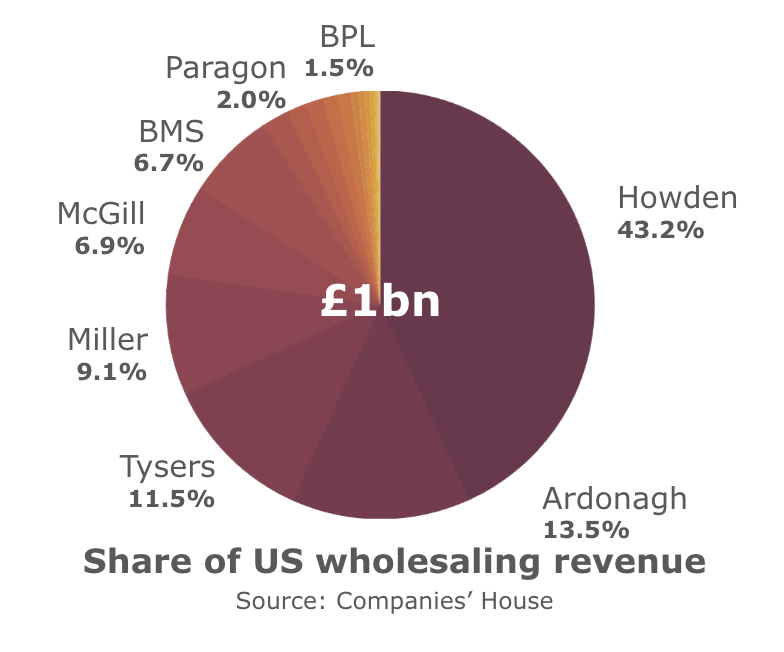

Based on a reading of their Companies’ House filings, I think that independent London brokers made about £1bn in fees on US business in 2022. That market is dominated by just four firms: Howden, Ardonagh, Miller and Tysers, each of which are sponsor-backed, and who collectively make up over 75% of the US-London wholesale market.

Howden and Ardonagh each have over £5bn in debt. Just last month, Ardonagh struck a £1.2bn deal for the Australian PSC Grouop, which includes Paragon, one of the last London independents. Time will tell how this story ends, but both of them are very levered. Here are some of the other recent transactions in the London broking market:

One of the dynamics to watch here is Howden and Ardonagh eyeing US expansion. Typically you see American brokers buying English ones - most notably with the acquisition of Bowring’s, a storied London broker, by Marsh in 1980. There are cases where it goes the other way: notably, Cooper Gay’s ill-fated acquisition of Swett and Crawford, which was subsequently folded into CRC, but also with the way Willis, originally an English firm, merged with the Americans. If Howden do choose to enter the US, they’ll have to do it with a bang: it’ll easily be a multi-billion dollar deal, not least because it will cannibalise their relationships with their other US clients. There’s a first-mover disadvantage here - if Howden wants to compete with its clients, Ardonagh will be more than happy to take them off their hands.

I’ve already covered some of the content in this piece elsewhere; but to wrap this up, I think three things are particularly interesting:

First, there’s the tension between the firm and the individual. People are the lifeblood of any brokerage; headcount makes up roughly 60% of costs, and bring in all the revenue. Whenever a broker describes itself as ‘entrepreneurial’, that means “we don’t tell you who to trade with”. But how do you keep your team happy, letting them use their unique skills and relationships, while also planning high-level corporate strategy?

Second, there’s the incessant jockeying for position between these firms - and there’s more to tell than I’ve been able to. In this piece, I’ve not focused on insurer relationships, or on non-US business, let alone the opportunity for creativity on the reinsurance side. Each opportunity brings concomitant risks, because most deals involve shutting someone else out.

Third, and perhaps most importantly, is the role of private equity in all this. Most of the firms listed above are privately-held. At the highest level, management moves freely. The founder and CEO of Aquiline is Jeff Greenberg, former CEO of Marsh and son of legendary AIG CEO Hank Greenberg; Dan Glaser, who spent 10 years running Marsh, is now at CD&R; David Howden is perhaps most of all a genius financier.

And so the rise (and potential fall) of the world’s largest broking firms is not entirely determined by client service and operating expertise; as Cicero had it in the Fifth Philippic, “the sinews of war are infinite money.”